EXECUTIVE SUMMARY

The Great Recession and its aftermath have adversely impacted the operations of nonprofit organizations (Nonprofit Finance Fund 2011) at the very time that demand for services is increasing. This circumstance, and recognition that the current economic downturn may be of extended duration, has prompted renewed discussion of how nonprofit organizations might create economies of scale through innovative business combinations.

While the scale of individual nonprofit organizations may have little relevance to solving some social problems (John Kania Winter 2011), it is an important and timely consideration in the evolution of the fragmented behavioral health and social services industry. Changes in the industry’s operating environment are harbingers of rapid consolidation, especially within the fragmented nonprofit provider sector. These changes include differences in the way services are delivered and financed, shifts in legislation and regulation, consumer preferences and provider leadership. This new environment presents the typical undercapitalized nonprofit human service provider with the need to provide an expanded array of often technology-enabled services, under an unfamiliar, at-risk contractual arrangement, frequently during a period of executive transition. These challenges have been exacerbated by the economic downturn, which has given rise to an intense provider rivalry encouraged by payors seeking to reduce costs.

As in other industries, these circumstances encourage industry consolidation and hence, the evolution of a market for corporate control. Yet very few nonprofit organizations possess the capital, competencies or experience required to execute a consolidation strategy. Furthermore few are in a position to develop the required capabilities due to structural and other barriers associated with traditional nonprofit business models. These models have historically been program-centric and differentiated primarily as a consequence of their size, as measured by annual revenues.

Clearly, a new business model is needed for the new paradigm; one that enables nonprofit organizations to adapt to the Industry’s greater demands and the emerging market for corporate control, without sacrificing core values. The goals of the new business model will be rapid growth supported by improved governance and new mechanisms for accumulating capital. The measure of its success will be unprecedented compound annual growth rates of revenues and net assets resulting from business unit expansion across a broad geography and range of human services.

A PRIMER ON NONPROFITS

A PRIMER ON NONPROFITS

Nonprofit organizations are a creation of state law, whereas tax exemption is primarily a function of federal tax law. Tax-exempt status confers two potentially significant benefits on nonprofit organizations: they pay no taxes with respect to net income on charitable activities, and donors may deduct contributions to most tax exempt-entities. To secure a nonprofit designation and tax exemption status, nonprofit organizations agree to serve one or more specified public purposes, and accept a prohibition on the distribution of profits which must instead be reinvested to further the organization’s charitable purpose. Nonprofit organizations have no owners, and are self-governing bodies.

The absence of an ownership interest has at least two significant effects on the operation of nonprofit organizations: it limits access to capital since there are no equity investors, and it dilutes governance by impairing ownership’s traditional role as a constraint on management’s pursuit of private interests. The limited access to capital further hinders the Industry’s nonprofit providers’ ability to invest in facilities, technology, management and working capital. It also handicaps the capacity to finance participation in Industry consolidation. As a result of these restrictions, nonprofit providers have grown almost exclusively through de novo development, and there are no national nonprofit consolidators. This evolution of the nonprofit sector has concurrently served the interests of nonprofit managements who have demonstrated a predictable reluctance to pursue the scale economies associated with business combinations, at the risk of their own personal positions.

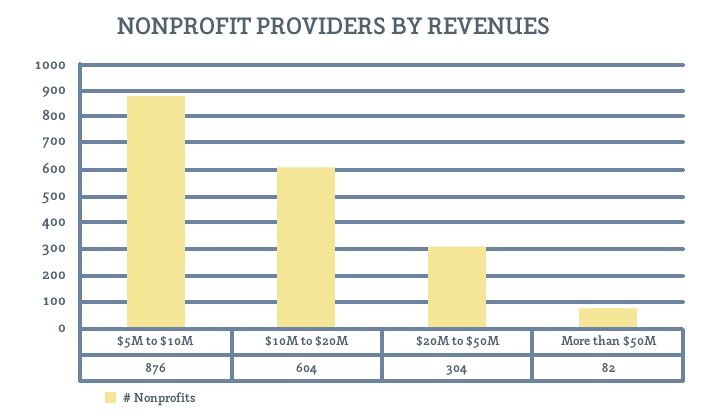

As a consequence, the nonprofit segment of the Industry remains fragmented. A search of the form 990 tax returns for 2009 in the Guidestar database reveals approximately 1,900 nonprofit human services providers with revenues of $5 million or more. The distribution of these nonprofits by annual revenues is presented in Figure 1.

Figure 1. Nonprofit Providers by Revenues.

While these circumstances would seemingly pave the way for Industry consolidation led by for-profit providers, this outcome has been thwarted by multiple obstacles. Foremost among these issues is the widespread belief among nonprofit trustees that the profit motive is incompatible with the mission of providing behavioral health and social services, compounded by a preference of many public officials and payors for nonprofit providers. Absent financial distress, these factors have often precluded nonprofit providers from responding to business combination proposals from for-profit consolidators – and there have been no nonprofit consolidators. Thus, nonprofit governance confronts a situation in which it has been unable to achieve scale in an industry entering maturity, yet unable to exit due to a self-imposed absence of a market for corporate control. The resulting excess capacity in the maturing industry suppresses the margin expectations of would-be consolidators, whether nonprofit or for-profit. This outcome isn’t serving the public interest; however, this recognition has initiated a variety of public policy responses.

These public policy responses have included the introduction of new forms of incorporation by various state governments. A low-profit limited liability company, or “L3C,” is a legal form of business entity created to bridge the gap between non-profit and for-profit investing by providing a structure that facilitates investments in socially beneficial, for-profit ventures. To date L3C legislation has been adopted in nine states. Another alternative enacted in seven states is the “B Corporation,” which also combines elements of for-profit and nonprofit corporate forms. Other proposed innovations include social impact bonds and the C3SOP® (see the accompanying article describing C3SOPs in this issue). Each of these reactions is intended to address the capital access limitations inherent in the nonprofit corporation structure, ultimately enabling nonprofits to achieve critical mass while reducing unit service costs.

PREVAILING NONPROFIT BUSINESS MODELS

PREVAILING NONPROFIT BUSINESS MODELS

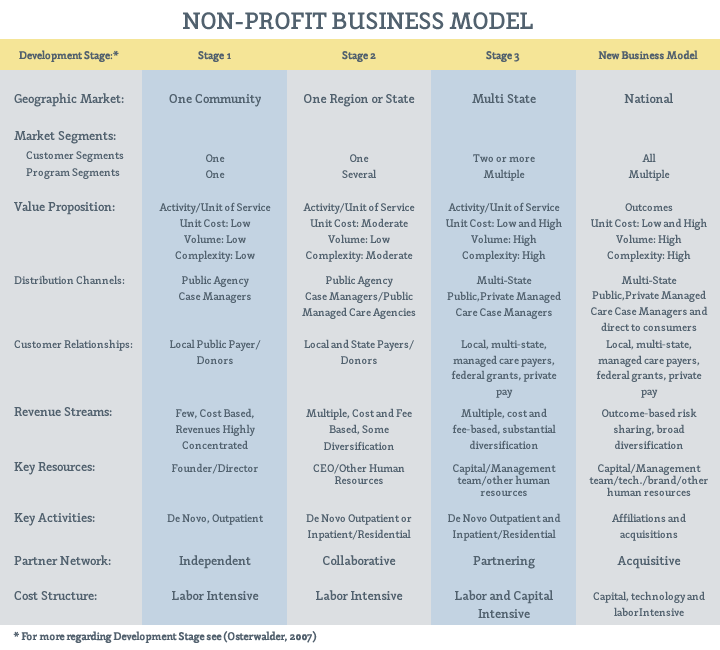

The industry’s nonprofit business models have historically been program-centric, and differentiated primarily as a consequence of their size, as measured by annual revenues. As a result, providers typically transition from one generic business model (Osterwalder 2007) to another in three phases as summarized in Table 1.

The Phase I business model is typical of nonprofit human services providers with revenues of less than $10 million. These providers characteristically offer a single service within a single community (e.g., an outpatient behavioral health service or residential service for developmentally disabled persons) that is funded by a single public payor, such as a county Department of Human Services. Individuals or families receiving service might be referred by a public agency case manager and likely do not present with multiple chronic conditions, and can likely be served at low cost. These providers most often will have limited histories and capital, and fees are often earned under low-risk, cost-based contracts. Many Phase I providers are led by their founders, who often possess additional product-related expertise.

Phase II providers include those with revenues of $10 million to $50 million. These providers have evolved to offer several services (e.g., behavioral health and substance abuse outpatient services, or residential and vocational services for developmentally disabled persons) regionally or statewide, and are funded by a several public payors. Individuals or families receiving service might be referred by public agency case managers or managed care organizations, and some of these clients have service needs of moderate complexity, entailing moderate expense. These providers may have histories of ten years or more but still lack significant capital due to revenues derived under a combination of cost-and fee-based contracts. Many providers transition to leadership by non-founders in the course of Phase II.

Phase III providers include the largest and best-capitalized providers. This structure offers a broad array of services for children, adults and families .in multiple states, and may be funded by numerous public and private payors. Individuals or families receiving service might be referred by public agency case managers and Medicaid and private-managed care organizations. These providers typically have long histories and have likely accumulated substantial capital, much of which is invested in real estate. Revenues are earned from many payors, and diversification of revenue streams has been a key driver of corporate strategy.

The typical Phase I organization structure consists of a single nonprofit tax-exempt enterprise that houses both service operations and fundraising, if the organization engages in any formal fundraising effort. Phase II organizations frequently incorporate a separate charitable foundation to administer fundraising efforts and to separately house the net capital accumulated by the development effort. Phase III providers usually adopt a holding company structure that includes multiple nonprofit providers, each a de novo venture established to address some unmet community need, and typically focused on a

specific program. The venture may even operate in several different states. In these Phase III organizational structures, the parent company frequently operates as a management company in an effort to benefit from scale economies.

This evolution of organizational structures has little impact on capital accumulation but significant impact on nonprofit governance. The decision to create a Foundation in Phase II adds significantly to the aggregate number of nonprofit enterprise trustees. Expanded board participation becomes unwieldy as Phase II operations become more complex, giving rise to trustee term limits during the Phase when organizational founders are succeeded by professional managers. Trustee term limits tend to exacerbate the information asymmetry between nonprofit trustees and nonprofit management, increasing agency costs. The commercial world’s antidote to agency costs – a market for corporate control – has not been operational in the Industry historically, but the changing Industry environment offers a catalyst. Payors increasingly demand integrated services that provide better outcomes at lower costs, and these demands are enforced through risk-sharing contracts that require larger, better-capitalized providers.